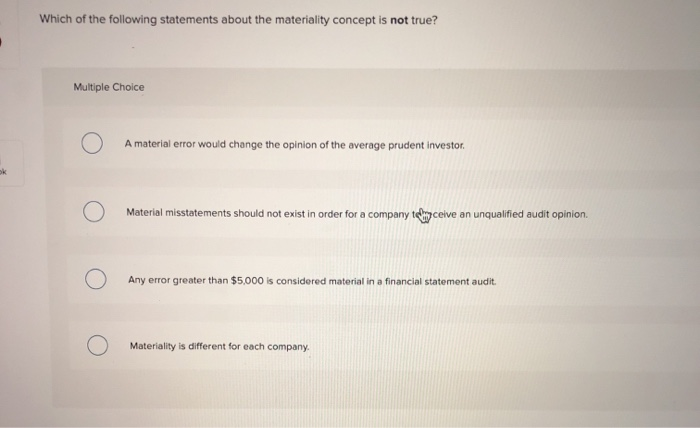

Which of the Following Statements About Materiality Is Not True

If performance materiality is set too low the auditor might not perform sufficient procedures to detect material misstatements in the financial statements. Materiality is determined by reference to.

Solved Which Of The Following Statements About The Chegg Com

Materiality is different for each company.

. Auditors are required to prepare a written audit plan during the planning stages of initialaudits but are not required to do so in continuing auditsb. Audit teams consider materiality in planning the audit performing the audit and evaluating the effect of misstatements on the entitys financial statementsc. If performance materiality is set too high the auditor might perform more substantive procedures than necessary.

Which of the following statements concerning materiality is true. If performance materiality is set too high the auditor might perform more substantive. Ii Is not an obligatory piece of legislation.

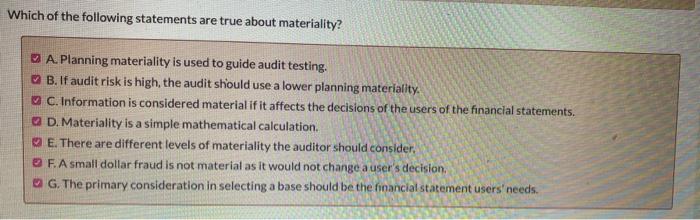

The concept of materiality recognizes that some matters are important for fair presentation of financial statements in conformity with GAAP while other matters are not important. MRP has evolved as the basis for Enterprise Resource Planning MRP provides a clean structure for dependent demand O MRP uses a bill-of-material inventory expected receipts and a master production schedule to determine material requirements O MRP is an independent demand. Affects only items reported in the income statement.

Conflicts of interest often occur between absentee owners and managers. B II only. All of these answers are correct.

Which of the following statements about the materiality concept is not true. Material misstatements should not exist in order for a company to receive an. C Materiality depends on the nature of an item but not on the dollar amount of the item.

B Performance materiality refers to the amounts set by the auditor at higher than the. The concept of materiality recognizes that some matters are important for fair presentation of financial statements in conformity with GAAP while other matters are not important. Audit evidence will comprise source documents and accounting records underlying financial statements and corroborating information from other sources.

Which one of the following statements is correct concerning the concept of materiality. A Materiality is determined by reference to specific quantitative guidelines established by the AICPA. Material misstatements should not exist in order for a company to receive an.

I Sets out who the users of the accounts are and how it is to be used. This Mora which is the. Any error greater than 5000 is considered material in a financial statement audit.

It was formed when very little progress was being made in terms of reformulating the structure of accounting theory. Preliminary materiality is the maximum amount by which the auditor believes the financials. It was formed at a time when the APB was under heavy criticism.

The concept of materiality. Genshin Impact 25 A Thousand Questions With Paimon Answers Revealed. Justifies ignoring the matching principle or the realization principle in certain circumstances.

Auditing is a type of attest service. B Materiality depends only on the dollar amount of an item relative to other items in the financial statements. Which of the following statements are true.

Which of the following statements about performance materiality is NOT true. Which of the following statements is not true with respect to the performance principlea. Which of the following statements is not true regarding the Trueblood Committee.

Decision makers demand reliable information that is provided by accountants. A Thousand Questions With Paimon is a recurring event in Genshin Impact that requires players to answer questions regarding the open-world RPG and rewards players with 50k Mora once per day upon answering all the questions correctly. In assessing the risk of material misstatements the audit team considers the effectiveness of the entitys internal controls in preventing and detecting misstatementsd.

Which of the following statements is NOT true about Material Requirement Planning. C both I and II. Performance materiality is essentially the same as overall materiality.

Each year the Financial Accounting Standards Board FASB publishes the dollar amount considered material for each industry. Statements regarding preliminary materiality are true. Generally accepted accounting principles are violated if estimates are used in end-of-period adjustments.

1 point Materiality depends on the nature of an item rather than the peso amount. D the sum of all the performance materiality levels can not exceed the preliminary judgment about materiality. Which of the following statements about materiality is not true.

D neither are true. An auditor considers materiality for planning purposes in terms of the largest aggregate level of misstatements that could be material to any one of the financial. Preliminary materiality may change during the engagement.

Auditing services and attestation services are the same. Treats as material only those items that are greater than 2 or 3 of net income. C Only ii and iii is true.

An accounting Conceptual Framework. A material error would change the opinion of the average prudent investor. A material error would change the opinion of the average prudent investor.

If performance materiality is set too ow the auditor might not perform sufficient procedures to detect material misstatements in the financial statements. Materiality is a matter of relative size or importance. An item is material if its inclusion or omission would influence or change the judgment of a reasonable person.

B only overstatements need to be considered. AAll of the above is true Only. Iii Defines concepts such as going concern relevance and materiality.

Which of the following statements about materiality is correct. Multiple Choice Materiality is different for each company. C professional judgment is critical.

In general the more misstatements the auditor expects the higher should be the aggregate materiality threshold. Any error greater than 5000 is considered material in a financial statement audit. Audit teams consider materiality in planning the audit performing the audit and evaluating the effect.

Could be misstated and still not affect the decisions of reasonable users. Information asymmetry seldom occurs. A Performance materiality is used to reduce the risk that the aggregate of uncorrected and undetected misstatements exceeds materiality for the financial statements as a whole to an acceptable level.

An auditors consideration of materiality is influenced by the auditors perception of the needs of a reasonable person who will rely on the financial statements. Aggregate materiality thresholds are a function of the auditors preliminary judgment concerning audit risk. A it is easy to predict in advance which accounts are most likely to be misstated.

A I only. Performance materiality is set less than overall materiality and helps the auditor determine the extent of audit evidence to obtain. B i is true.

An item must make a difference or it need not be disclosed. Which of the following statements concerning materiality thresholds is incorrect.

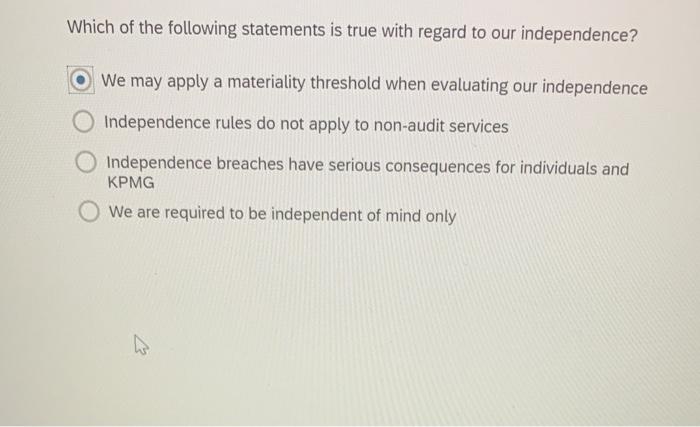

Solved Which Of The Following Statements Is True With Regard Chegg Com

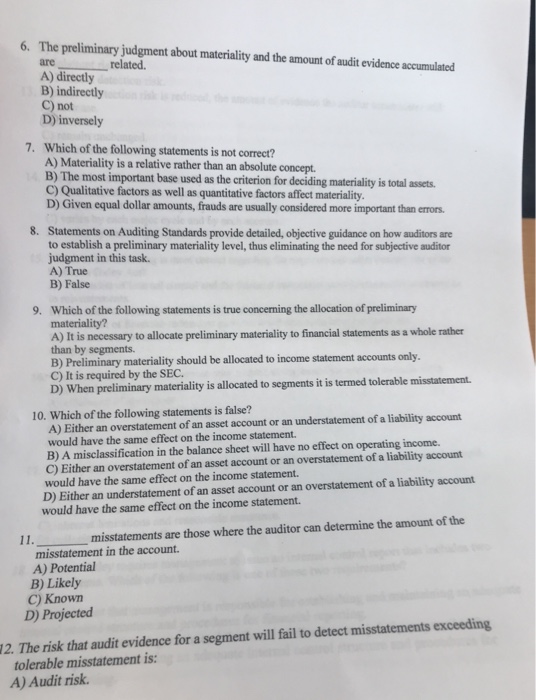

Solved 6 The Preliminary Judgment About Materiality And The Chegg Com

Solved Materiality Is An Important Aspect Of Any Audit Chegg Com

No comments for "Which of the Following Statements About Materiality Is Not True"

Post a Comment